“You think hemophilia doesn’t apply to your plan and you don’t have to pay attention, but what happens when it does? You need to be ready to put plan design changes in place now. Being proactive means less disruption.”

- MBGH Employer Member

Alternative Funding Programs (AFPs)

Alternative funding programs (AFPs) have emerged as a cost containment strategy for employers and vendors, but the patient experience reveals a very different reality—one defined by delays, denials, and negative financial and clinical consequences. AFPs operate in one of two ways – by either carving out hemophilia medications entirely, leaving the patient with no coverage options, or by denying the medications at point of authorization and rerouting to the AFP vendor.

Patients or providers receive a denial, representing the only alternative as enrollment in a manufacturer's 340B patient assistance program (PAP). This flips the intent of PAPs on its head: instead of serving as a safety net for patients facing genuine affordability barriers, PAPs become a mandatory workaround for insured members whose coverage has been intentionally withdrawn. For many patients, AFPs introduce an intermediary process that is confusing and difficult to navigate.

The patient experience is often defined by delay and uncertainty. Vendors themselves acknowledge the AFP process can take days, weeks or even months before a patient receives medication—an unacceptable gap for individuals with serious or chronic conditions. Members also face increased complexity in their benefit design, with multiple handoffs, unclear instructions, and shifting points of contact. These administrative hurdles can translate directly into clinical risk. Delayed access to therapy has been repeatedly flagged as a driver of worsening symptoms, avoidable complications, and long term health consequences. For conditions like hemophilia, where treatment timing is critical, even short interruptions can lead to emergency department visits, joint damage, or other irreversible harm.

Financially, AFPs introduce additional layers of instability. Specialty drug rebates may be lost entirely because carved out utilization is rebate ineligible. Many members will not qualify for PAPs in the first place leading to 34% of them paying the full cost of the medication because many self insured members exceed income thresholds, leaving them without any viable path to treatment. Meanwhile, AFP administrators collect substantial fees— up to 30% of the medication's list price — and PBM administrative fees often rise as well.

These costs accumulate even as patients face higher out of pocket burdens. High cost share is strongly associated with nonadherence, treatment abandonment, and disease progression. Financial toxicity—emotional and psychological distress caused by medical expenses—further compounds the burden, particularly for low wage workers. Patients often report they are often unaware accumulators or maximizers are being applied until a pharmacist informs them at the point of sale.

Accumulator Adjusters and Maximizers

When a copy accumulator is applied, the manufacturer copay assistance does not count towards the patient’s deductible or out-of-pocket maximum so when the assistance runs out, the patient is responsible for the full remaining cost share.

The copay maximizer spreads the value of the manufacturer’s copay card across the full year. The employer’s plan sets the patient’s monthly cost-share equal to the maximum monthly value and the patient typically pays zero. The employer captures the full value of the manufacturer’s assistance and maximizers keep the drug in the plan.

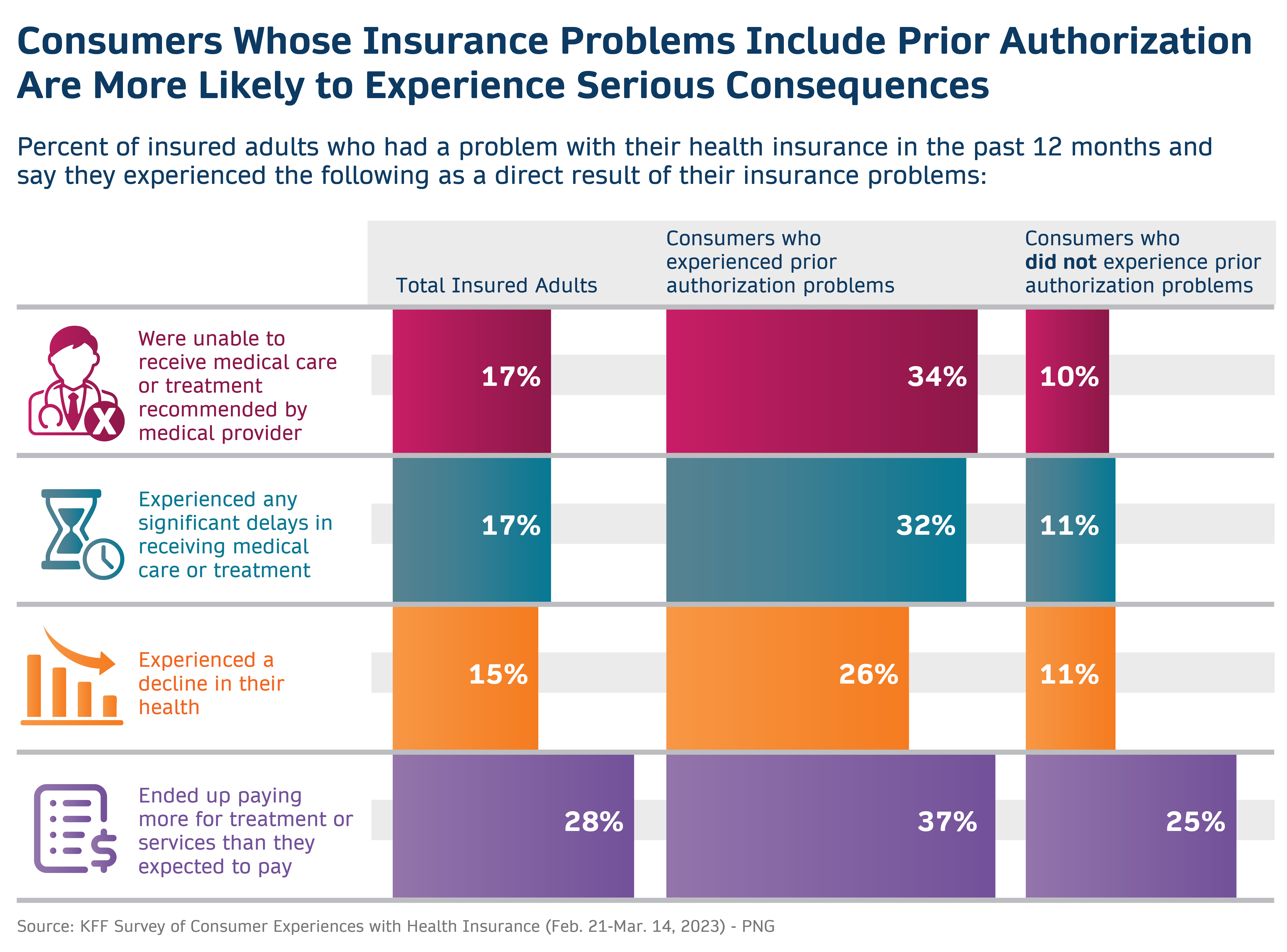

Prior Authorization

According to the Journal of Managed Care and Specialty Pharmacy, the intent of prior authorizations is to ensure that drug therapy is medically necessary, clinically appropriate, and aligns with evidence-based guidelines. The reality for rare disease patients is that these tactics delay care, lead to both patient and clinician frustration, and are rarely denied.

Coverage Denials

Coverage denials add yet another layer of friction. Roughly 15% of all claims submitted to private payers are initially denied, including many that had already cleared prior authorization. Denials disproportionately affect higher cost therapies, with the average denied claim tied to charges of $14,000 or more. While more than half of these denials are ultimately overturned, it only happens after multiple rounds of appeals—each costing providers an average of $43.84 per claim. Nationally, this administrative churn consumes nearly $20 billion annually. For patients, these delays and reversals translate into treatment interruptions, uncertainty, and avoidable clinical deterioration.

Taken together, AFPs, high cost sharing mechanisms, and coverage denials create a fragmented and often hostile experience for patients who rely on specialty therapies. Instead of improving affordability, these strategies frequently shift costs, increase administrative burden, and jeopardize continuity of care. The result is a system where insured patients can find themselves without access to the medications they need, facing delays that carry real health consequences, and navigating a benefit design that feels more like an obstacle course than a support structure.

AFPs impact employers as well. Twenty-nine percent of members report they considered leaving their employer because of inadequate insurance coverage and 13% did leave their employer. AFPs may expose employers to legal liabilities such as discrimination and ERISA and medical loss ratio violations which can be extremely costly.

Employers: There can be unintended consequences of delayed care from the benefit plan design itself. For life-saving drugs, these delays can result in negative health outcomes as well as additional costs to the plan.